{kind=link}

Prediction market anomaly monitor for detecting potential insider trading on politically-sensitive Kalshi markets.

Built in response to the George Santos/Kalshi investigation (June 2026) and the broader question: what can be detected from public API data alone?

pmwatch continuously monitors Kalshi prediction markets where participants may have material nonpublic information (MNPI) -- cabinet departures, SCOTUS resignations, AG nominations, geopolitical actions, and economic data releases -- and flags anomalous trading patterns before public announcements.

It is a tipping-point detector, not an identity resolver. It finds markets where something looks wrong. Kalshi and the CFTC use their internal data (account IDs, KYC records) to do the actual investigation. pmwatch surfaces the candidates.

On February 23, 2026, George Santos publicly posted he would attend the State of the Union. He had already placed bets on Kalshi that he would not attend. When he didn't show up, the odds cratered and he profited tens of thousands of dollars.

Kalshi caught him using internal account data. pmwatch detects the market-level pattern:

- Large position established before a public statement that moves prices significantly

- Volume Z-score spike against historical baseline

- Directional price movement inconsistent with public information

The Santos detection didn't require user identity -- it required noticing that someone already knew something the market didn't.

pmwatch monitors 33 high-MNPI-risk series across five categories:

| Category | Series | MNPI Risk Actors |

|---|---|---|

| Executive Actions | KXCABOUT, KXNEXTAG, KXNEXTDEF, KXNEXTSTATE, KXNEXTODNI... | WH chief of staff, personnel office |

| SCOTUS | KXSCOTUSRESIGN, KXSCOURT, KXTARIFFS... | Justices, clerks, Senate judiciary |

| Economic Data | KXFED, KXCPI, KXGDP | FOMC members, BLS/BEA staff |

| Geopolitical | KXGREENTERRITORY, KXCANAL, KXZELENSKYPUTIN... | NSC, State Dept, DoD |

| Congressional | KXIMPEACH, KXHOUSE, KXSENATE, KXGOVSHUT... | Congressional leadership, whips |

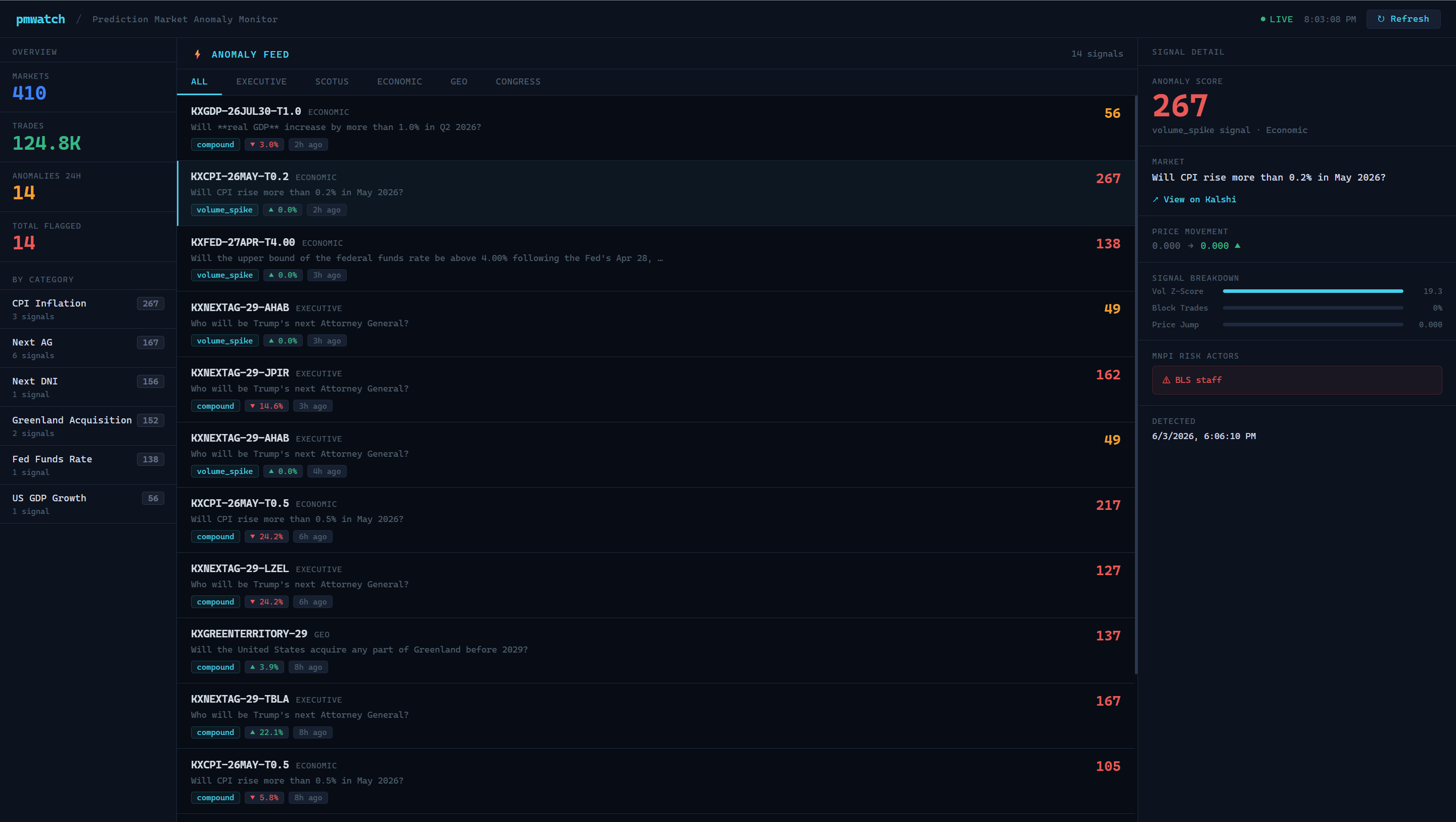

Each market is scored using three signals:

1. Volume Z-Score Compares recent trade volume to a rolling baseline. A spike of 8+ standard deviations above normal baseline is a strong anomaly signal.

2. Block Trade Ratio

Large privately-negotiated contracts on politically-sensitive markets are a red flag.

Block trades are identified via the is_block_trade field in the Kalshi API.

3. Price Divergence Detects sudden directional price movement not explained by gradual drift -- the signature of someone positioning ahead of an announcement.

Compound score = (max(0, vol_z - 1.5) * 15 * block_modifier) + price_bonus

Thresholds: Yellow >= 25, Red >= 60.

A single anomaly can be noise. A series of anomalies on the same market over hours or days is a pattern.

Sophisticated actors don't establish large positions at once -- they accumulate slowly, in sub-threshold increments, staying under the noise floor. The Santos case was sloppy. A more careful actor would look like a sequence of moderate anomalies on the same market, each unremarkable individually, building toward a larger position before an announcement.

pmwatch detects this via gap-based clustering: anomaly events on the same market within a 72-hour window are grouped into a cluster and scored together.

Cluster scoring factors:

- Anomaly count — how many distinct anomaly events in the window

- Directional consistency — are all the block trade anomalies on the same side (YES or NO)? Consistent direction suggests one actor accumulating rather than random noise.

- Score trend — are the anomaly scores escalating over time? Increasing urgency suggests growing conviction ahead of an event.

- Peak score — the strongest individual signal in the cluster

Cluster score = peak × (1 + consistency) × (1 + escalation) × log(count)

The Clusters tab in the dashboard shows all active clusters sorted by cluster score.

| Market | Score | Signal | MNPI Risk |

|---|---|---|---|

| KXNEXTAG-29-TBLA | 167 | compound | WH personnel office |

| KXNEXTODNI-29-RCRA | 156 | compound | WH personnel office |

| KXGREENTERRITORY-29 | 152 | compound | NSC, State Dept |

| KXCPI-26MAY-T0.5 | 105 | compound | BLS staff |

Note: high scores do not imply insider trading. They flag markets warranting closer examination.

On June 3, 2026 — pmwatch's first live run — the Kalshi market

KXNEXTAG-29-TBLA generated three escalating anomaly scores tied to

trading on who would be President Trump's next Attorney General.

| Market | Score | Time (ET) | MNPI Risk |

|---|---|---|---|

| KXNEXTAG-29-TBLA | 118 | 11:35:49 a.m. | WH personnel office |

| KXNEXTAG-29-TBLA | 167 | 12:04:12 p.m. | WH personnel office |

| KXNEXTAG-29-TBLA | 377 | 9:27:56 p.m. | WH personnel office |

Later that day, President Trump said during a White House dinner that he

would nominate Acting Attorney General Todd Blanche to serve as attorney

general on a permanent basis, according to subsequent reporting that

described the remarks as occurring Wednesday evening. The ticker suffix

TBLA corresponds directly to Blanche's initials.

pmwatch first detected anomalous activity in this market at 11:35:49 a.m. ET (score 118), followed by a stronger alert at 12:04:12 p.m. ET (score 167). Both signals occurred well before public reporting of the White House dinner remarks and were associated with upward price movement, elevated volume, and a risk profile linked to the White House personnel process.

A third, more concentrated burst of unusual activity was detected at 9:27:56 p.m. ET, with a materially higher anomaly score of 377. This late-evening spike is temporally close to the dinner remarks, but the exact time of Trump's statement is not clearly documented in public coverage, so this case study does not claim minute-level alignment.

Source: AP, ABC News, NBC News, and other major outlets reporting on President Trump's June 3, 2026 statement that he would nominate Todd Blanche as attorney general.

This is pmwatch's first documented detection. The tool identified unusual activity in a politically sensitive market in late morning and early afternoon, well before the president's Wednesday evening remarks were publicly reported, and then flagged a second, sharper anomaly at approximately 9:28 p.m. ET.

On June 3, 2026 — pmwatch's first live run — the Kalshi market

KXNEXTAG-29-TBLA generated three escalating anomaly scores tied to

trading on who would be President Trump's next Attorney General.

| Market | Score | Time (ET) | MNPI Risk |

|---|---|---|---|

| KXNEXTAG-29-TBLA | 118 | 11:35:49 a.m. | WH personnel office |

| KXNEXTAG-29-TBLA | 167 | 12:04:12 p.m. | WH personnel office |

| KXNEXTAG-29-TBLA | 377 | 9:27:56 p.m. | WH personnel office |

Later that day, President Trump said during a White House dinner that he

would nominate Acting Attorney General Todd Blanche to serve as attorney

general on a permanent basis. The ticker suffix TBLA corresponds directly

to Blanche's initials.

pmwatch first detected anomalous activity at 11:35:49 a.m. ET (score 118), followed by a stronger alert at 12:04:12 p.m. ET (score 167). Both signals occurred well before public reporting of the White House dinner remarks and were associated with upward price movement, elevated volume, and a risk profile linked to the White House personnel process.

A third, more concentrated burst of unusual activity was detected at 9:27:56 p.m. ET, with a materially higher anomaly score of 377.

The cluster scorer groups all three events into a single cluster with a cluster score of 785 — 3 anomalies, escalating, over a 10-hour span.

Source: AP, ABC News, NBC News, and other major outlets reporting on President Trump's June 3, 2026 statement that he would nominate Todd Blanche as attorney general.

This is pmwatch's first documented detection. The tool identified unusual activity in a politically sensitive market in late morning and early afternoon, well before the president's Wednesday evening remarks were publicly reported, and then flagged a second, sharper anomaly at approximately 9:28 p.m. ET. The cluster score of 785 makes this the strongest pattern in pmwatch's history.

watchmarket_watchlist.json # 33 monitored series with MNPI risk annotations

collector.py # Polls Kalshi API every 60 min, stores trades + candlesticks

scorer.py # Z-score + block trade + price divergence anomaly detection

cluster_scorer.py # Gap-based clustering of anomalies; directional + trend scoring

db.py # SQLite schema and query helpers (anomalies + clusters tables)

scheduler.py # APScheduler wrapper: collect → score → cluster, every 60 min

api.py # FastAPI backend serving dashboard and JSON endpoints

dashboard.html # Single-file dark-mode monitoring UI with Clusters tab

GET /api/anomalies # Recent anomaly events, sorted by time

GET /api/clusters # Active clusters sorted by cluster_score

GET /api/market/{ticker}/clusters # Cluster history for a specific market

POST /api/clusters/refresh # Re-run cluster scorer on demand

GET /api/markets # All watched markets with current price/volume

GET /api/stats # Summary stats and category breakdown

GET /api/market/{ticker}/trades # Raw trade history for a market

| Limitation | Impact |

|---|---|

| No user identity in public data | Cannot name who placed trades |

| No order placement timestamps | Only fill time is available |

| Historical API depth ~3 months | Limited retroactive analysis |

| Kalshi only | Polymarket (offshore) has separate API |

git clone https://github.com/lweiss01/pmwatch.git

cd pmwatch

pip install -r requirements.txt

python db.py # initialize database (creates anomalies + clusters tables)

python scheduler.py # start collection + scoring loop (runs every 60 min)

uvicorn api:app --port 8000 # start dashboard API

Requires Python 3.10+. No API key needed -- all endpoints used are public.

- Anomaly scoring (volume Z-score, block trade ratio, price divergence)

- Gap-based cluster analysis with directional consistency and trend scoring

- Clusters tab in dashboard with pattern interpretation

- Timeline drill-down: individual anomaly events within a cluster

- Government calendar integration (BLS release schedule, FOMC dates)

- Social media correlation (cross-reference X posts with trade anomalies)

- Email/webhook alerts on high cluster scores

- Polymarket support

- Resolve candidate initials in market tickers to full names

- NPR: DOJ investigating George Santos for insider trading on Kalshi

- Congress.gov: Prediction Markets and Insider Trading Law

- H.R. 7004: Public Integrity in Financial Prediction Markets Act of 2026

- Kalshi API Documentation

pmwatch is a public transparency tool. It detects market-level anomalies using only publicly available data. It does not identify individual traders, make accusations, or constitute legal or financial advice. High anomaly scores indicate unusual market activity that may warrant further investigation -- nothing more.